To make Wealthtender free for readers, we earn money from advertisers, including financial professionals and firms that pay to be featured. This creates a conflict of interest when we favor their promotion over others. Read our editorial policy and terms of service to learn more. Wealthtender is not a client of these financial services providers.

➡️ Find a Local Advisor | 🎯 Find a Specialist Advisor

[In this guest article, Carroll Golden and Dan Mangus offer a fresh perspective on Medicare and a caregiving system that increasingly relies on unpaid, multigenerational support. They examine the “Shadow Caregiving System and Economy,” the convergence of Medicare and retirement planning, and strategies for integrating these insights into practice management. By focusing on practical approaches rather than academic analysis, Golden and Mangus provide readers with research and tools for understanding the essential role of Medicare and caregiving in comprehensive retirement planning.]

As the landscape of caregiving, Medicare, and retirement planning evolves, clients increasingly face health crises and complex decisions that impact their retirement strategies. Changing Medicare rules, rising costs, and shifting supplemental insurance options – compounded by the repeal of the Chevron Doctrine – add financial strain across generations, leading to a natural convergence between Medicare and retirement planning.

Clients are adjusting their investment strategies and retirement savings in anticipation of potentially supporting themselves or their parents’ pre- and post-retirement medical expenses. The need for potential adjustments is heightened by the increasing reality of longer lifespans.

With these issues growing in importance for a broadening client base, financial advisors now navigate a complex web of challenges. They work to find effective strategies for clients moving through pre- and post-retirement phases, many of whom are also shouldering care for aging parents. Advisors must make a strategic choice: integrate Medicare-related services into their offerings or rely on outside expertise.

The State of Caregiving in America

A previous article by Carroll Golden offers details on the Shadow Caregiving System explaining that in the US, caregivers provide over 95% of informal care and cites a recent report, Valuing the Invaluable, which vividly depicts the current state of family caregiving in the U.S. The report indicates that: “In 2021, about 38 million family caregivers in the United States provided an estimated 36 billion hours of care to adults with limitations in daily activities. The estimated economic value of their unpaid contributions was approximately $600 billion.”

Most caregivers share a common experience: they often start and continue their caregiving roles without any formal training or a clear understanding of how demanding the role can become. Many are unaware of the available support services, insurance options, or that Medicare does not cover long-term care needs. Many also do not realize that their parent’s retirement income impacts certain aspects of Medicare and may influence the type of Medicare they elect and the type of supplement they purchase.

Clients are themselves either caregivers or care recipients. Although many parents may plan to rely on Medicare to cover healthcare costs, Medicare does not generally cover long-term care – including in-home care services – that millions of aging Americans may require. So, what does that mean for aging clients or clients with aging parents?

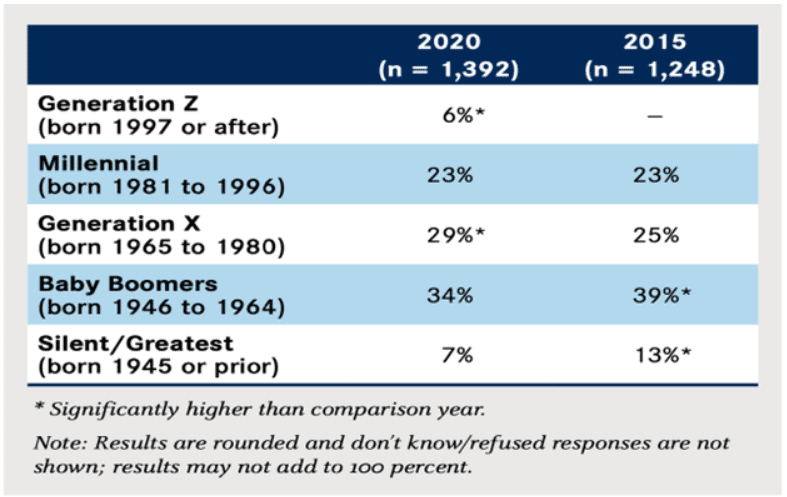

A recent study, Caregiving in the U.S. 2020, indicates that the generational makeup of the Shadow Caregiving System is shifting. In a few short years, from 2015 to 2020, caregiving responsibilities shifted away from older generations to younger generations. No doubt the trend will continue.

The implications of the shadow caregiving system and economy are clearly multigenerational. Goldman Sachs research indicates that no matter the age of the client, caregiving can impact finances. Moreover, for advisors and agents who want to attract Gen Xers or millennials as clients, it is important to note that 63% of Gen Xers and 79% of millennials expect caregiving and associated financial demands to undermine their own progress toward retirement goals. And 55% of Gen Xers and 72% of millennials predict that they will lose earnings and career momentum due to caregiving.

The Sandwich Generation

PEW research offers some further financial implications of caregiving and “the sandwich generation.” It indicates that just under 50% of caregivers are considered “sandwich generation” caregivers as they simultaneously raise children while caregiving for aging parents and in some cases, grandparents. Members of this generation often find themselves torn between their work responsibilities, caregiving duties, and parenting obligations. The pressures of caring for aging parents, managing financial responsibilities, and handling emergencies can significantly reduce the time available for personal and professional activities.

A survey conducted by AgingCare.com found that most family caregivers are vastly unprepared for covering these costs. The survey found that 63% of family caregivers have no plan as to how they will pay for their parents’ care over the next five years. As a result, caregivers admitted that the cost of caring for a parent has impacted their own ability to plan for their own financial future. Additionally, 72% predict that they will lose earnings and career momentum due to caregiving. It is crucial and eye-opening information for financial professionals who need to factor in the cost of healthcare across generations in their planning models.

Regardless of income, advisors and agents encounter questions from clients and their children that seem straightforward at first glance, such as: What if I don’t need Medicare? Can I get Medicare? When can I get Medicare? How much will Medicare cost? However, these seemingly simple questions have complex answers, as clients differ in age, income, and work status. There is an online tool available on Medicare.gov. By searching for “estimate cost” on the homepage, advisors can find a page titled “Estimate My Medicare Eligibility and Premium.” By inputting a client’s specific responses to a set of questions, this tool helps determine their eligibility and premium costs.

Whether financial professionals discuss the impact of healthcare and specifically caregiving or not, across all generations, the fact remains that many clients’ earning power, and by extension their ability to save for retirement, is and will continue to be impacted.

Health Savings Accounts

More consumers are enrolling in Health Savings Accounts (HSA) which are a type of tax-advantaged savings account available to consumers enrolled in High Deductible Health Plans (HDHPs). HSA assets have soared by a factor of 22 between 2006 and 2023 to $123 billion as the share of workers using employer-sponsored plans that have high-deductible health insurance plans jumped from 7% to 31%. HSA funds can be used to help pay their deductibles, some premiums, co-payments, and co-insurances amounts. However, there are some key things advisors need to know about how Medicare works with HSA accounts when clients may ask about them. For example, if a client enrolls in Medicare Part A and/or B, they can no longer contribute pre-tax dollars to their HSA. In fact, they need to stop contributing to the HSA at least 6 months prior to enrolling into Medicare or they may incur a tax penalty.

It is also important to note that if clients choose to delay Medicare enrollment because they are continuing to work and want to continue to contribute to their HSA, they must also delay their Social Security benefits.

State Actions on Medicaid and Long-term Care

Some people may qualify for free or low-cost health care through Medicaid based on their income and family size. If their income and resources are below the required levels, then a person may be considered “dual-eligible” qualifying for both Medicare and Medicaid. Medicaid would then help cover expenses not covered by Medicare like nursing home care or home-based services. State qualifications vary depending on residence.

State Medicaid budgets are the dominant source of payment for long-term care, followed by out-of-pocket payments by individuals and families. The increasing cost-of-care incurred by Medicaid state budgets is not sustainable. Individual states are in various stages of tackling the growing needs and resulting expenditures for our older and disabled population. More and more states are actively engaged in proposing legislation, creating a task force, conducting a study, or funding for a study, etc.

Medicare and Medicaid are large complex programs. But they are extremely important and represented 26% of federal program spending in fiscal year 2023. Sooner or later, clients will ask about these programs.

Integration of Health and Wealth

In today’s world, financial professionals are serving clients who are living longer, which brings both opportunities and challenges. However, many overlook the impact on both caregivers and care recipients who are caught in the shadow caregiving economy. Even the best-designed retirement plans can be seriously disrupted if the ongoing and evolving costs of healthcare post-retirement are not factored in. To successfully navigate extended lifespans, integrating health and wealth planning is essential.

To best serve clients, a basic understanding of Medicare as a primary source of health insurance for retirees requires understanding enrollment periods, coverage options, and costs is vital.

Medicare.gov provides tools, information, and publications built for consumers who need Medicare assistance. As an advisor you will also find CMS.gov helpful as it is built for the health care community. Using the tools and information on that site gives you a behind the scenes look at what CMS is building/distributing as they provide coverage to more than 100 million people through Medicare, Medicaid, The Children’s Health Insurance Program (CHIP) and The Health Insurance Marketplace. There are three that should be especially helpful:

- “Understanding Medicare Advantage Plans” Medicare publication number 12026

- “Choosing a Medigap Policy” Medicare publication number 02110

- “Beneficiaries Dually Eligible for Medicare & Medicaid” ICN: MLN006977

Medicare Supplement plans help cover costs that Medicare does not, such as copayments, coinsurance, and deductibles. There is an increasing number of enrollees who have switched to Medicare Advantage plans. Enrollees have experienced increasing premiums of their Medicare Supplements, and that Medicare Advantage plans offered lower premiums and added benefits like dental vision and some even had perks like gym memberships. Of course, there was an exchange for those benefits.

Medicare Advantage plans change each year; they have co-pays, and coinsurance amounts and have networks of providers that must be utilized. The potential annual changes present a less predictable cost environment especially for clients dealing with chronic or serious illness. On Medicare.gov review “Compare Original Medicare & Medicare Advantage.” to get a better handle on helping on a client’s unique circumstances.

Medicare Advantage: An alternative to traditional Medicare, Medicare Advantage Plans offers additional benefits but require careful comparison. Medicare premiums, Medicare drug plans, and Medicare Advantage plans all change at the beginning of each year. Medicare Advantage and Medicare Part D drug plans are annual contracts that insurance carriers make with CMS that reset on January 1 of each year. The annual enrollment period that runs from October 15th to December 7th each year.

In Conclusion

To reinforce the significance that medical and long-term care expenses have on retirement planning, refer to Lincoln Financial Group’s findings from a 2023 Survey of Financial Professionals and Consumers. The survey indicates that medical and long-term care expenses are seen by consumers as bigger threats to a retirement portfolio than longevity, inflation, or the economy.

The Shadow Caregiving System will continue to grow. We are now in ‘Peak 65” years with more than 11,000 people turning 65 every day. Medicare decisions will increasingly become part of the planning process. There are two different but equally effective approaches to incorporating Medicare into financial professional practices. Advisors need to choose to either integrate Medicare-related services or strategically partner with a trusted Medicare resource to benefit your clients.

This article was originally published here and is republished on Wealthtender with permission.

About the Author

Bill Hortz

Founder Institute for Innovation Development

Bill Hortz is an independent business consultant and Founder/Dean of the Institute for Innovation Development- a financial services business innovation platform and network. With over 30 years of experience in the financial services industry including expertise in sales/marketing/branding of asset management firms, as well as, creatively restructuring and developing internal/external sales and strategic account departments for 5 major financial firms, including OppenheimerFunds, Neuberger&Berman and Templeton Funds Distributors. His wide ranging experiences have led Bill to a strong belief, passion and advocation for strategic thinking, innovation creation and strategic account management as the nexus of business skills needed to address a business environment challenged by an accelerating rate of change.